Polyethylene Weekly: The high-pressure rally has slowed down, and the two markets are now in range turmoil, waiting for new drivers to emerge

The core point of the week

This week, the range of China's PE market is sorted out, with prices fluctuating up and down from 50 to 150 yuan per ton. As of Thursday, China's linear prices were 7700-8050 yuan / ton; high-voltage film prices were 8300-8550 yuan / ton; low-voltage film prices were 7950-8900 yuan / ton; and low-voltage wiredrawing prices were 7870-9950 yuan / ton. In June and July, PE is in the gap period of new production capacity and production expansion, and the number of new parking devices has increased in the past two days, and it is mainly high-pressure devices, but the early parking devices start-up and resume work to a certain extent cover the output loss caused by the new parking devices. From the downstream point of view, the current traditional demand off-season, the terminal operating rate is low, and there are generally insufficient orders, weak profits, the market demand is difficult to vibrate. However, with the improvement of market macro expectations, market speculative demand and early short order cover increased, the overall transaction is better than the previous period. In the future, under the fact that the fundamentals have not changed greatly, we will pay more attention to the intensity of China's stimulus policy and the feedback of commodities on macro expectations and reality.

Chapter one, Review of Polyethylene Market this week

1. Analysis of the market trend of polyethylene in China

Unit: yuan / ton

|

Brand number |

Region |

June ninth |

June fifteenth |

Rise and fall |

|

Linear |

North China |

7730-7850 |

7770-7850 |

40/0 |

|

East China |

7900-8050 |

7900-8050 |

0/0 |

|

|

South China |

7950-8100 |

7900-7950 |

-50/-150 |

|

|

high pressure |

North China |

8500-8550 |

8500-8550 |

0/0 |

|

East China |

8350-8500 |

8300-8450 |

-50/-50 |

|

|

South China |

8350-8400 |

8300-8400 |

-50/0 |

|

|

Low pressure membrane material |

North China |

8200-8900 |

8200-8900 |

0/0 |

|

East China |

8200-8900 |

8200-8900 |

0/0 |

|

|

South China |

7950-8900 |

7950-8900 |

0/0 |

|

|

Low pressure wire drawing |

North China |

8000-9500 |

7870-9550 |

-130/50 |

|

East China |

8000-9350 |

8050-9350 |

50/0 |

|

|

South China |

9350-9900 |

9350-9950 |

0/50 |

This week, the range of China's PE market is sorted out, with prices fluctuating up and down from 50 to 150 yuan per ton. Since this week, Shanghai, Daqing, China Sea Shell, Lanhua and other devices have stopped, and the overall supply has shrunk, especially in terms of high pressure. While Sinopec for high-pressure factory prices frequently pull up, the corresponding cost support on the floor has also been enhanced. Returning to the overall market, the overall pressure on petrochemical inventory during the week is not great, inventory remains fluctuating around 70, and the ex-factory prices of the two oil are relatively strong. Coal companies, affected by the decline in coal prices and futures at the beginning of the week, reduced prices, and then followed the market rebound to repair the previous decline. In addition to the adjustment of fundamentals, due to the introduction of various policies and data between China and the United States, the macro impact of the market has intensified. Although futures intra-day, daytime volatility increased, but the whole still around 7500-7820 front-line box shock, did not come out of the trend market. However, with the second half of the week, market expectations have improved, market speculative demand has picked up slightly, low-price transactions have increased during the week, downstream still maintain rigid demand. As of Thursday, China's linear prices were 7700-8050 yuan / ton; high-voltage film prices were 8300-8550 yuan / ton; low-voltage film prices were 7950-8900 yuan / ton; and low-voltage wiredrawing prices were 7870-9950 yuan / ton.

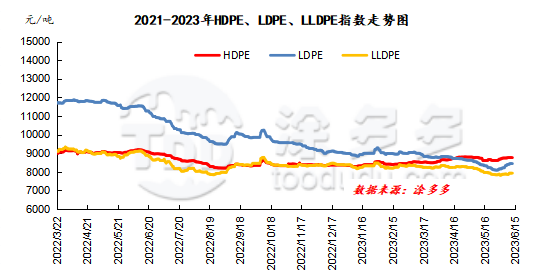

Figure 1 polyethylene sub-variety index trend chart

2. Analysis of the market trend of polyethylene dollar

This week, the trend of China's US dollar PE market is stronger than that of China's RMB market. Most of the varieties rose 10-30 US dollars per ton last Friday, so it is difficult for prices to continue to rise this week. Import arrivals have increased this week, especially high pressure in the Middle East and North America. The transaction situation is still difficult to increase, and the export performance is also mediocre. From the point of view of the price difference between inside and outside, the window of high-voltage and low-pressure film products is open, while other categories are closed. In the near future, foreign businessmen will announce new prices one after another, and judging from the prices known yesterday, foreign prices have declined steadily. Pay attention to the new quotations made by foreign businessmen and the trend of RMB market.

Table 2 & changes of nbsp; polyethylene market price in US dollars

Unit: United States dollars / ton

|

Variety |

June ninth |

June fifteenth |

Rise and fall |

|

Linear |

930 |

920-940 |

-10/10 |

|

high pressure |

940 |

940-960 |

0/20 |

|

Low pressure membrane material |

950 |

960-980 |

10/30 |

3. Analysis of the trend of polyethylene futures market

The main plastic cubicle runs this week. The L2309 contract opened at 7748 on June 9, with a weekly high of 7834, a weekly low of 7609, and closed at 7789 on Thursday. In terms of Thursday's transaction: 21.6% more, 23.2% empty, while Duoping was at 19.9% and 21.8%. At present, the L09 contract BOLL (135013) runs around the interval between the upper and lower tracks, focusing on 7820 pressure at the top, support near 7500 at the bottom and breakthroughs at the bottom.

Chapter II Analysis of the supply of Polyethylene in China

The shutdown of Daqing Petrochemical, Lanzhou Petrochemical, Dushanzi Petrochemical and other plants led to the decline of capacity utilization of Chinese polyethylene production enterprises. This week's capacity utilization rate is 81.6%, down 5.05% from the previous cycle.

Table 3 overhaul statistics of polyethylene plants in China

Unit: ten thousand tons

|

Enterprise name |

Inspection and repair device |

Maintenance capacity |

Parking Duration |

departure time |

|

North China brocade |

Old HDPE first line / second line |

15 |

June 12, 2014 |

Long-term parking |

|

Shenyang Chemical Industry |

LLDPE |

10 |

October 15, 2021 |

Uncertain for the time being |

|

Haiguolong oil |

Full density |

40 |

April 3, 2022 |

Uncertain for the time being |

|

Wanhua chemistry |

HDPE |

35 |

November 12, 2022 |

Uncertain for the time being |

|

Liaoyang Petrochemical Company |

HDPE A line |

3.5 |

April 1, 2023 |

June 15, 2023 |

|

Liaoyang Petrochemical Company |

HDPE B line |

3.5 |

April 1, 2023 |

June 15, 2023 |

|

Fushun petrochemical |

Full density |

8 |

April 6, 2023 |

June 30, 2023 |

|

Daqing Petrochemical |

HDPE B line |

8 |

April 27, 2023 |

July 1, 2023 |

|

Shanghai Secco |

Full density |

30 |

May 19, 2023 |

July 14, 2023 |

|

Daqing Petrochemical |

LDPE first line |

6.5 |

May 20, 2023 |

July 25, 2023 |

|

Shanghai Secco |

HDPE |

30 |

May 21, 2023 |

July 17, 2023 |

|

Lanzhou Petrochemical |

Old total density |

6 |

June 1, 2023 |

July 20, 2023 |

|

Lanzhou Petrochemical |

HDPE old line |

8.5 |

June 1, 2023 |

July 20, 2023 |

|

Lanzhou Petrochemical |

HDPE new line |

8.5 |

2023 |

July 20, 2023 |

|

Zhejiang Petrochemical Phase II |

Full density |

45 |

June 6, 2023 |

June 16, 2023 |

|

Shanghai Sinopec |

LDPE2 |

5 |

June 9, 2023 |

June 14, 2023 |

|

Daqing Petrochemical |

LLDPE |

8 |

June 10, 2023 |

July 25, 2023 |

|

Daqing Petrochemical |

HDPE A line |

8 |

June 10, 2023 |

July 25, 2023 |

|

Daqing Petrochemical |

HDPE C line |

8 |

June 10, 2023 |

July 25, 2023 |

|

Daqing Petrochemical |

LDPE second line |

20 |

June 10, 2023 |

July 25, 2023 |

|

Daqing Petrochemical |

Full density front line |

30 |

June 10, 2023 |

July 25, 2023 |

|

Daqing Petrochemical |

Full density second line |

25 |

June 10, 2023 |

July 25, 2023 |

|

Yanshan Petrochemical |

The old LDPE front line |

6 |

June 12, 2023 |

June 15, 2023 |

|

China Shell Phase II |

HDPE |

40 |

June 12, 2023 |

June 15, 2023 |

|

Lanzhou Petrochemical |

New full density |

30 |

June 12, 2023 |

August 4, 2023 |

Chapter III demand Analysis of Polyethylene in China

3.1 downstream market analysis of polyethylene

The agricultural film market is weak this week. As of Thursday, the mainstream price of double-protective film in North China was 9100-10000 yuan / ton, the mainstream price in East China was 9300-10200 yuan / ton, and the mainstream price in South China was 9200-10200 yuan / ton. Agricultural film production is traditionally off-season, orders are scarce, most enterprises shut down for maintenance, other enterprises stage production, agricultural film enterprises are expected to maintain low demand for PE raw materials in the later stage.

3.2 Statistics on the operating rate of downstream polyethylene enterprises

capacity utilization in downstream industries this week is 0.37% lower than last week. The utilization rate of agricultural film capacity decreased by 0.28% compared with last week. The utilization rate of pipe capacity is down 0.50% from last week. The utilization rate of hollow capacity increased by 0.12% over last week, and that of packaging film increased by 0.10% compared with last week.

Chapter IV & Analysis of the upstream market of nbsp; polyethylene

4.1 crude oil trend analysis

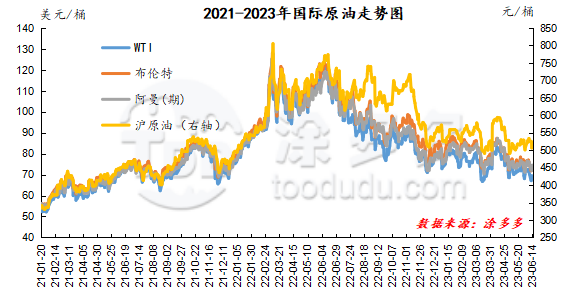

As of June 14, the price of WTI was $68.27 per barrel, down $3.02 from the same period last week; Brent was $73.20 per barrel, down $2.76 from the same period last week; Oman (period) was $74.54 per barrel, down $1.55 from the same period last week; Shanghai crude oil was 521.1 yuan per barrel, down 12.4 yuan per barrel compared with the same period last week.

Figure 2 international crude oil trend chart

4.2 methanol trend analysis

Recently, the price of raw material coal is weak and stable, and the cost support is insufficient. At present, the supply in the field is still abundant, and Longxingtai's new 300000-ton methanol plant has been put into operation smoothly, and the supply is expected to continue to increase, but the raw material inventory of some downstream enterprises is on the high side. The mood of manufacturers to take goods continues to be depressed. Although some production enterprises have lowered their quotations for shipment, the buying mentality is still bearish, and the demand margin may be significantly improved in the short term. The trading atmosphere in the market is slightly depressed. In the port market, futures market volatility is strong, spot rigid demand negotiations, the basis is slightly weaker, so far, the port regional inventory performance is different, East China is affected by part of the time closure, the overall unloading speed is general, the mainstream area pick-up is stable, thus showing a narrow range of depots, but although there is normal consumption downstream in South China, imports and domestic trade vessels have arrived at Hong Kong during the week, resulting in a narrow stock accumulation in the region. At present, the macro performance of the methanol market is poor, the contradiction between supply and demand still exists, and the pessimism of the operators in the market continues to be strong. It is expected that the price of methanol market will be weak in the short term, and we need to pay attention to the prices of crude oil and coal and the operation of the plant in the field in the later stage.

Chapter 5 & Forecast of the trend of nbsp; Polyethylene

In June and July, PE is in the gap period of new production capacity and production expansion, and the number of new parking devices has increased in the past two days, and it is mainly high-pressure devices, but the early parking devices start-up and resume work to a certain extent cover the output loss caused by the new parking devices. From the downstream point of view, the current traditional demand off-season, the terminal operating rate is low, and there are generally insufficient orders, weak profits, the market demand is difficult to vibrate. However, with the improvement of market macro expectations, market speculative demand and early short order cover increased, the overall transaction is better than the previous period. In the future, under the fact that the fundamentals have not changed greatly, we will pay more attention to the intensity of China's stimulus policy and the feedback of commodities on macro expectations and reality.