- Mall

- Supermarket

- Supplier

- Cross-Border Barter

- Industrial Data

- Warehouse Logistics

- Trade Assurance

- Expo Services

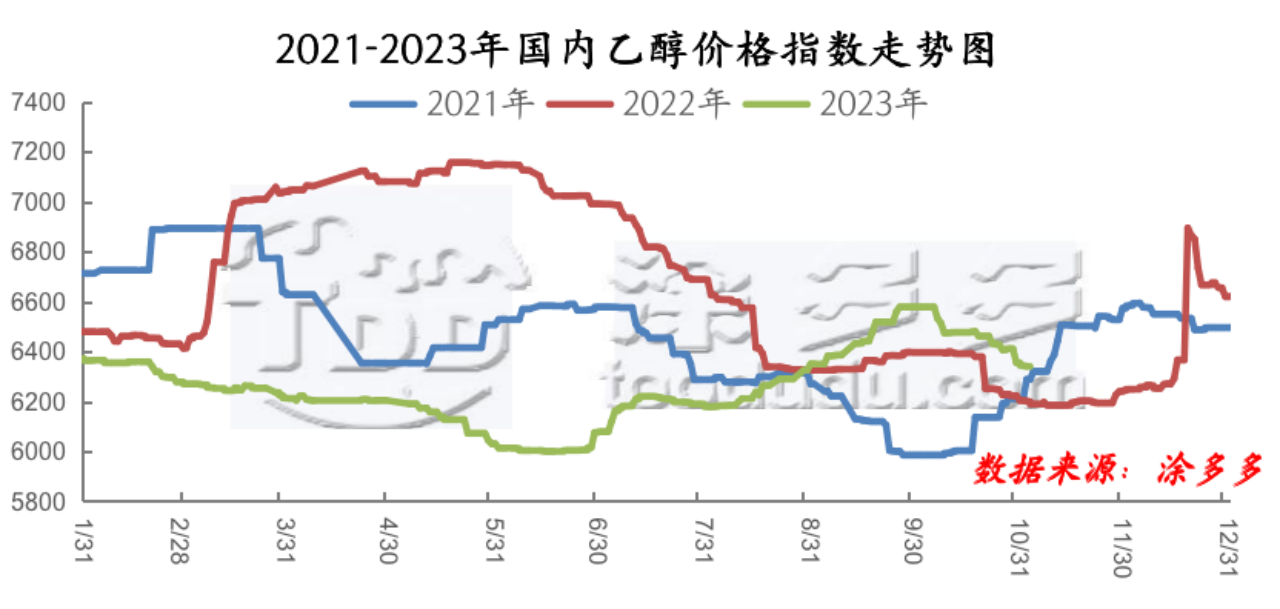

On November 3rd, the price index of general-grade ethanol was 6339.25, up from-1.5 on the previous working day.

& nbsp; the price region of China's ethanol market weakens. November 3 hot spots: first, Henan excellent individual quotations continue to be reduced by 50 yuan / ton. Second, the price in East China will be reduced by 50 yuan per ton. Third, the price in Northeast China is stable and the order is delivered. 4. The bidding price of ethyl acetate has been reduced obviously. Fifth, fuel prices are weak. Sixth, the purchasing price of regional georefining is weak.

Specifically, prices in Northeast China are stable, chemical orders are shipped, and shipments to East China are increasing. The prices of some superior factories in Henan are weak and their shipments are weak. Some factories in East China have shut down, but the demand is general, and the quotations of the main factories have been lowered. Fuel prices are weak. The earth refinery is sent to the price weak finishing. Northeast enterprise Jilin market price 6400-6500 yuan / ton, Jilin no water 7100-7300 yuan / ton. The general grade of Heilongjiang market is 6250-6400 yuan / ton, and the Heilongjiang anhydrous market is 7050-7250 yuan / ton. The northeast closing position is about 6650-6750 yuan / ton. The superior enterprises in Central China offer 6750-6800 yuan / ton, and the water-free price is 7450-7700 yuan / ton. The price of ethanol in East China is 6750 yuan / ton. The price of anhydrous ethanol is 7500-7600 yuan / ton, and the general price in southern Jiangsu is 7000-7100 yuan / ton. Cassava ethanol & nbsp;7050-7200 yuan / ton in Guangxi, South China.

& nbsp; unit: yuan / ton

|

Area |

Specifications |

Market |

2023/11/3 |

2023/11/2 |

Rise and fall |

|

|

South China |

Cassava is anhydrous |

Guangxi |

7850-7950 |

7850-7950 |

0/0 |

|

|

Molasses 95% |

Guangxi |

- |

- |

- |

|

|

|

Cassava 95% |

Guangxi |

7050-7200 |

7200-7200 |

-150/0 |

|

|

|

North China |

Superior grade |

Hebei |

- |

- |

- |

|

|

No water |

Hebei |

7300-7400 |

7300-7400 |

0/0 |

|

|

|

Northeast China |

General level |

Jilin |

6400-6500 |

6400-6500 |

0/0 |

|

|

No water |

Jilin |

7100-7300 |

7100-7300 |

0/0 |

|

|

|

General level |

Jinzhou |

6650-6750 |

6650-6750 |

0/0 |

|

|

|

General level |

Heilongjiang Province |

6250-6400 |

6250-6400 |

0/0 |

|

|

|

East China |

General level |

Anhui Province |

- |

- |

0/0 |

|

|

No water |

Anhui Province |

7650-7650 |

7650-7650 |

0/0 |

|

|

|

No water |

Shandong |

7500-7550 |

7500-7550 |

0/0 |

|

|

|

General level |

Shandong |

6750-6800 |

6750-6800 |

0/0 |

|

|

|

Superior grade |

Shandong |

6850-7050 |

6850-7050 |

0/0 |

|

|

|

Send it to other places without water. |

Shandong |

7400-7400 |

7400-7400 |

0/0 |

|

|

|

General level |

Northern Jiangsu |

6750-6750 |

6800-6800 |

-50/-50 |

|

|

|

No water |

Northern Jiangsu |

7500-7600 |

7550-7650 |

-50/-50 |

|

|

|

General level |

Southern Jiangsu |

7000-7100 |

7000-7100 |

0/0 |

|

|

|

Central China |

Superior grade |

Henan |

6750-6800 |

6800-6800 |

-50/0 |

|

|

No water |

Henan |

7450-7700 |

7450-7700 |

0/0 |

|

Raw materials / by-products and downstream

Unit: yuan / ton, US dollar / ton

|

Area |

Market |

Raw materials / by-products |

2023/11/3 |

Remarks |

|

Northeast China |

Jilin |

Corn |

2350-2400 |

|

|

Northeast China |

Jilin |

DDGS |

2350-2450 |

|

|

Northeast China |

Heilongjiang Province |

Corn |

2298-2310 |

Less transactions at a low price |

|

Northeast China |

Heilongjiang Province |

DDGS |

2250-2300 |

High fat |

|

Central China |

Henan |

Corn |

2650-2690 |

|

|

Central China |

Henan |

DDGS |

2300-2350 |

|

|

Thailand |

|

Dried cassava |

275-279 |

|

|

Shandong |

|

Ethyl acetate |

6350-6390 |

Acceptance leaves the factory |

|

Jiangsu Province |

|

Ethyl acetate |

6450-6550 |

|

|

South China |

|

Ethyl acetate |

6550-6650 |

|

Future forecast: short-term weak consolidation of China's ethanol market, weak corn prices, negative costs, stable supply in Northeast China, order delivery, decline in start-up in East China, and delivery of goods from Northeast China to arbitrage, increased enthusiasm for purchasing goods from Northeast China. Large factories do not have obvious inventory, but the market bearish mentality is not conducive to the transaction of new orders. In Henan area, the thick source plant has a start-up plan in the middle of the year, and the supply is increased. At present, the chemical arbitrage is closed, and the inventory is likely to be weak. There is a decline in construction in East China, there are not many local sources of goods, some of them consume the sources of goods in Northeast China, the production costs of enterprises are high, the losses are serious, and the price reduction space of local sources is limited. Fuel ethanol market has low price, limited downstream demand and weak price arrangement. The construction of coal-based ethanol increased around the middle of the year, and the price is weak under the limited demand.

Raw material: corn ethanol: the price of Chinese corn is weak with the influence of the quantity, but the price has rebounded slightly recently. At present, the supply of ddgs is increasing, the demand is limited, and the price is weak this week. Cassava dry aspect: enterprise rigid demand procurement, Thailand is willing to raise the price is obvious, cassava dry inventory sales are expected short-term cassava dry price high finishing. The market is low in price and average in quality.

Supply: northeast start: Dongning Hongda shutdown, Baoquanling shutdown, Luobei production, Cofco Zhaodong normal, Wanli installation normal, Hongzhan 4 factories normal, Heilongjiang Shenglong production, Zhongkegreen production, Fuyu Huihai production; Fukang production, Tianyu production, Shuntong production, Dongfeng Huafeng production, Xintianlong normal, Liuniu production. Huadong Huatian production, Guannan shutdown, Jin Changlin downtime, Guohua shutdown, Changxing production, Longhe downtime, Romat production, sul shutdown, Fulaichun shutdown, Maibo Huihui shutdown, MINUSTAH production. Houyuan, Mengzhou, Henan Province, downtime, other normal. Jufeng shuts down. Chifeng Ruiyang production, Zhalantun production, Inner Mongolia Jietainuo plant production. Jilin fuel is normal, Guotou Tieling production. Tianguan Nanyang production. Guotou Jidong production. State Investment Helen production.

Demand: downstream chemical rigid demand procurement. Liquor order purchase.

Logistics: logistics price is stable.

Equipment maintenance table of Chinese ethanol enterprises

|

Enterprise name |

Production capacity (10,000 tons / year) |

Maintenance involves production capacity |

Maintenance start time |

Remarks |

|

Hongzhan (Jixian) |

60 |

60 |

April fifteenth |

Start up on May 6th |

|

Jilin Fukang |

50 |

4 |

March 28th |

|

|

Heilongjiang Hexing grain and oil |

3 |

3 |

Late March |

|

|

Inner Mongolia Shuntong |

12 |

12 |

Production on October 8th |

|

|

Heilongjiang Zhongke Green |

10 |

10 |

Production on August 30th |

|

|

Fulaichun, Shandong Province |

20 |

20 |

Stop the machine |

|

|

Jiangsu Dongcheng |

15 |

15 |

Stop the machine |

|

|

Guannan COVID-19, Lianyungang |

5 |

5 |

Stop the machine |

|

|

Jiangsu Haiyan |

15 |

15 |

Start up in the middle of May |

|

|

Jiangsu Maibo remittance |

8 |

8 |

Stop feeding at the beginning of April |

|

|

Shuyang Guohua |

5 |

5 |

Resume downtime in mid-August around July 10 |

|

|

Anhui COFCO |

75 |

30 |

It is expected to shut down in September on April 20th. |

|

|

Anhui Wuhechun |

8 |

8 |

Stop the machine |

|

|

Jilin Xintianlong |

30 |

30 |

Shut down on May 5, start on the 17th, reduce production on the 21st, full production on July 15th. |

|

|

Heilongjiang Sheng long |

15 |

15 |

Shut down on April 27-start on June 5, put in material from July 19 to September 16 |

|

|

Inner Mongolia Liniu |

10 |

10 |

October production |

|

|

Hanyong, Mengzhou, Henan Province |

30 |

30 |

One-line production |

|

|

Houyuan, Mengzhou, Henan Province |

50 |

50 |

Open on May 21 and shut down on October 26th |

|

|

Jilin Dongfeng Hua Grain |

10 |

10 |

Fire from 17 April to 9 October |

|

|

National Investment Helen |

30 |

30 |

April 12-May 24, September 20-September 26 |

Fuel fuel |

|

Guotou Jidong |

30 |

30 |

April 3rd |

Fuel fuel |

|

Zhenjiang Changxing |

10 |

10 |

All machines were shut down on May 16, June 5, July 19, August 28. |

|

|

Jin Changlin in Lianyungang |

5 |

5 |

Shutdown on May 18, production on August 7, shutdown around August 15. |

|

|

Hongzhang, ha. |

60 |

30 |

From 27 May to 20 July, Phase II from September 25 to October 9 |

|

|

Fukang |

50 |

50 |

Feed from August 10 to August 31 |

|

|

Tianyu |

15 |

15 |

Stop feeding on July 21 and feed on August 13 |

|

|

Cofco Zhaodong |

30 |

10 |

Stop feeding on June 5-June 20, July 15 stop fuel production on July 31, feed on August 15 |

|

|

Chifeng Ruiyang |

8 |

8 |

Shut down on June 10th and feed on July 4th. |

|

|

Hongzhan Tahiko |

30 |

30 |

Stop from June 20th to July 5th |

|

|

Wanli Runda |

60 |

60 |

Shutdown on July 15th and feeding on July 31st |

|

|

Lianyungang Longhe River |

10 |

10 |

July 3 device stop feeding August 21 feeding November 3 shutdown |

|

|

Jiangsu sul alcohol |

12 |

12 |

The device was shut down on July 3 |

|

|

Liaoyuan giant peak |

50 |

50 |

Production stopped on July 4th and August 1st. |

|

|

Zalantun |

10 |

10 |

The product will be released around July 6th. |

|

|

Shandong Yingxuan |

20 |

20 |

Shut down at the end of June and put in material on July 25. |

|

|

Jilin fuel |

70 |

70 |

The two lines will be inspected from 31 July to 20 August. |

|

|

Guotou Tieling |

30 |

30 |

The machine was shut down on July 31 for maintenance and put in the material on August 10. |

|

|

Henan Nanyang Tianguan |

30 |

30 |

August 15 put into production |

|

|

Romet. |

5 |

5 |

August 18 put into production |

|

|

Fuyu Huihai |

5 |

5 |

Downtime in mid-August-October 3 |

|

|

China Colleen |

10 |

10 |

Feeding starts on August 22nd |

|

|

Guotou Jidong |

30 |

30 |

Feed in early September |

|

|

Hongzhan Huannan |

30 |

30 |

October 08-October 22 |

|

Remarks: all estimated downtime and production capacity are subject to the specific downtime of the factory.