- Mall

- Supermarket

- Supplier

- Cross-Border Barter

- Industrial Data

- Warehouse Logistics

- Trade Assurance

- Expo Services

China Urea Price Index:

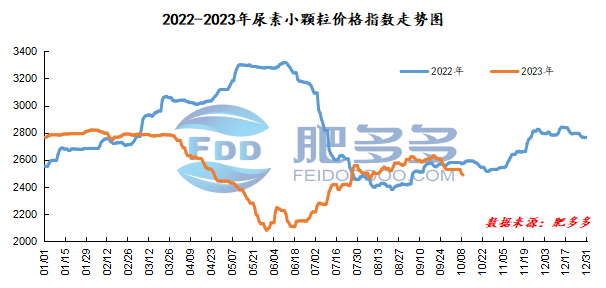

According to Feiduo data, the urea small pellet price index on October 9 was 2,487.27, down 10.91 from yesterday, down 0.44% month-on-month, and down 3.45% year-on-year.

Urea futures market:

Today, the opening price of the Urea UR2401 contract is 2118, the highest price is 2182, the lowest price is 2104, the settlement price is 2145, and the closing price is 2162. The closing price is 11% higher than the settlement price of the previous trading day, and the month-on-month increase is 0.51%. The daily fluctuation range is 2104-2182, and the price difference is 78; The 01 contract has increased its position by 14956 lots today, and so far, it has held 304028 lots.

Spot market analysis:

Today, China's urea market prices continue to maintain a downward trend. Currently, the overall market supply is high, downstream purchasing is cautious, and the market trading atmosphere continues to remain flat.

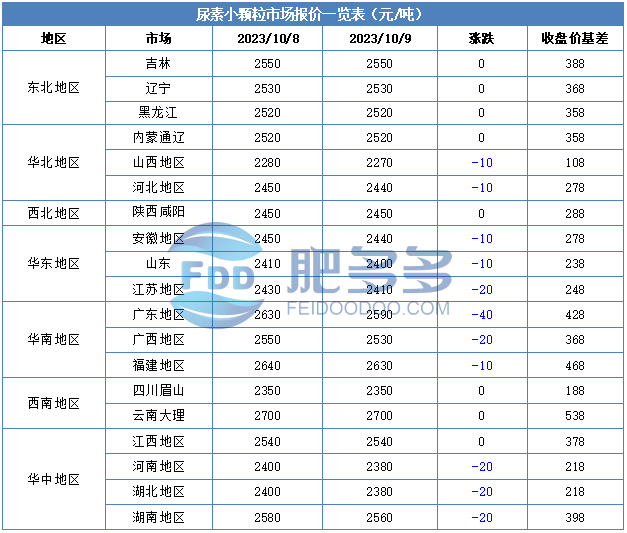

Specifically, prices in Northeast China have stabilized at 2,510 - 2,550 yuan/ton. Prices in North China fell to 2,270 - 2,450 yuan/ton. Prices in the northwest region are stable at 2,450 - 2,460 yuan/ton. Prices in Southwest China are stable at 2,350 - 2,800 yuan/ton. Prices in East China fell to 2,370 - 2,450 yuan/ton. The price of small and medium-sized particles in Central China fell to 2,370 - 2,640 yuan/ton, and the price of large particles stabilized at 2,470 - 2,510 yuan/ton. Prices in South China fell to 2,530 - 2,640 yuan/ton.

Market outlook forecast:

In terms of supply, maintenance equipment is still being restarted one after another, new production capacity is also being released, and market supply continues to remain at a high level. In terms of enterprises, enterprises currently mostly implement advance orders before the holidays. Due to the current market situation, enterprises are short of new orders transactions. Most enterprises with small orders are gradually lowering their ex-factory quotations in order to receive new orders. On the demand side, downstream demand has weakened, willingness to replenish goods is low, and a wait-and-see mentality is dominated. In terms of cost, the price of upstream synthetic ammonia is also gradually falling slightly, simultaneously driving changes in urea prices. Upstream coal prices are relatively firm, and port coal prices continue to increase after the holiday.

Overall, in terms of current market conditions, urea prices still have some downside space, so it is expected that the urea market price will continue to be dominated by a downward trend in the short term.